why state-led identity is the future

Welcome to our institutional newsletter, Crypto Long & Short. This week:

- Tricia Gallagher on how the fix for broken digital identity systems will need to be state-led and user-controlled.

- Top headlines institutions should pay attention to by Francisco Rodrigues.

- Crypto TCG gacha volumes hit all-time high as CARDS token surges 52% in Chart of the Week.

Thanks for joining us!

You’re reading Crypto Long & Short, our weekly newsletter featuring insights, news and analysis for the professional investor. Sign up here to get it in your inbox every Wednesday.

Expert Insights

Fighting fraud in the digital age: why state-led identity is the future

By Tricia Gallagher, founder and principal, Treasury Solutions Info Tech (TSIT)

The United States has lost an estimated $5 trillion to fraud and improper payments across government programs.

That number should stop us in our tracks.

Yet most policy responses still focus on detection, recovery and enforcement. They miss the underlying issue. Fraud at this scale is not a compliance failure — it is an infrastructure failure and at its center is identity. Addressing it requires a shift away from band-aid solutions toward a re-architecture of our digital identity framework.

There is a growing movement around the idea that identity — and control over access to personal data — belongs to the individual, not to banks, technology platforms or even the government. Even within the financial system, where data use is more tightly regulated, individuals often lack meaningful visibility or control. Data sharing operates through broad, one-time consent frameworks that enable ongoing access and reuse of financial data with limited transparency. More importantly, when consumers cannot actively direct how their data is shared and used, they are limited in their ability to access new and tailored financial services — constraining innovation, reducing competition and slowing economic growth.

This dynamic is even more pronounced in the technology sector, where personal data is routinely collected, aggregated and monetized at scale. Across both domains, individuals have limited awareness of who has access to their data and how it is used.

At its core, this model requires individuals to surrender control of their identity and personal data to participate. These systems are not only inefficient, they expand the surface area for misuse and security breaches. More fundamentally, they erode individual agency and undermine the very notion of inalienable rights in the digital age.

Two major policy debates in Washington reflect this tension: one focuses on reducing fraud and improper payments; the other centers on control of consumer financial data. They are treated as separate issues, but in reality reflect the same structural gap.

Policymakers are responding, but largely within the constraints of the current system. Congressional efforts to update the Gramm-Leach-Bliley Act focus on consumer data control through opt-in and opt-out regimes. At the same time, the Trump Administration has elevated fraud prevention through expanded oversight and increased data sharing across agencies. Since January 2025, more than a dozen federal initiatives — including an interagency fraud task force — have been launched.

On one side, policymakers are pursuing incremental privacy improvements. On the other, they are expanding access to sensitive government data to combat fraud. The result is continued reliance on centralized data pools, combined with limited individual control over how personally identifiable information (PII) is accessed and used. These architectures increase exposure, create attractive targets for bad actors and remain difficult to secure at scale.

The core challenge is not simply data protection. It is how to enable trusted verification and privacy while preserving individual control over access to personal data. Without that control, individuals are required to relinquish how their data is accessed and used, undermining a core inalienable right in the digital economy. This is where states have a critical role to play.

States have long served as the primary issuers of identity through birth records, driver’s licenses and other foundational credentials. This positions them to lead the next phase of digital identity infrastructure. The future of digital identity will require states to become the anchor of trust — not by expanding data collection, but by re-architecting how that trust is expressed: shifting from centralized data silos to privacy-preserving, user-controlled credentials.

Utah provides a clear example. Through legislation taking effect in May 2026, the state has introduced a Digital Identity Bill of Rights that places individuals at the center of how their identity is used and shared. It establishes clear principles to enable user control, data minimization, restricted surveillance and verification based only on what is necessary. At its core is a simple reality: trust in financial systems requires authoritative identity. Access to public funds and services depends on verified eligibility, and states already fulfill this role.

The goal is not to remove the state, but to modernize how trust is expressed. By shifting to privacy-preserving, user-controlled credentials, states can reduce fraud, improve transparency and strengthen accountability.

As federal debates continue to focus on managing data within legacy systems, states have an opportunity to lead in a fundamentally different direction — one that reduces reliance on centralized data and restores individual control over identity and personal information. The future of digital finance will not be defined by speed alone, but by whether systems uphold both trust and rights.

Identity is the bridge between the two.

Headlines of the Week

This week delivered a blend of significant developments across geopolitics, global regulation, and decentralized finance.

Stablecoins were a key focus globally, with the Federal Deposit Insurance Corp. formally proposing its approach to U.S. federal rules and a group led by HSBC and Standard Chartered receiving Hong Kong’s first stablecoin licenses.

Meanwhile, crypto entered geopolitical tensions as Iran explored collecting transit fees in cryptocurrency for oil tankers passing through the Strait of Hormuz. The Strait has since been blockaded by the U.S. navy.

Chart of the Week

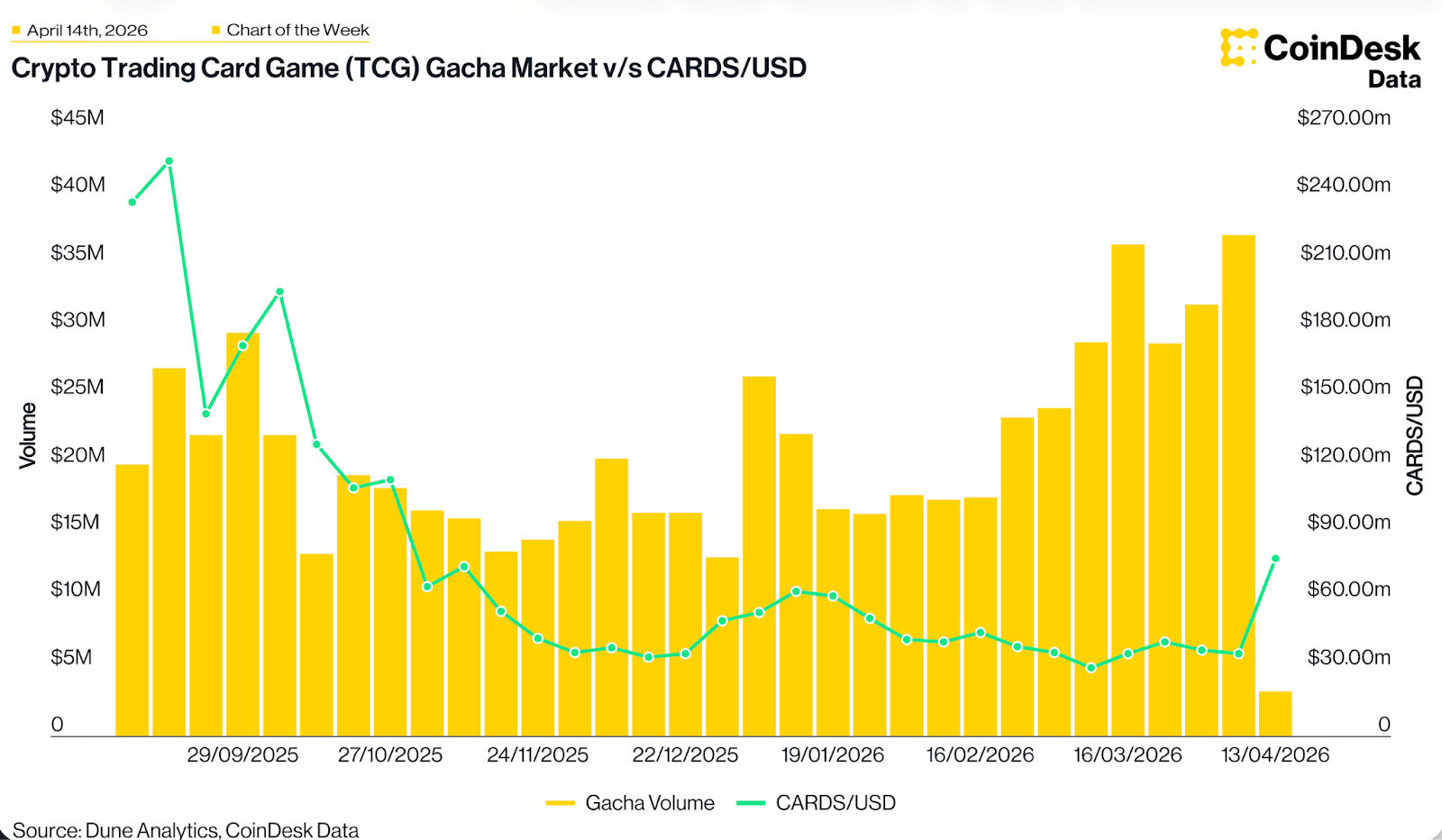

Crypto TCG gacha volumes hit all-time high as CARDS token surges 52%

The crypto Trading Card Game (TCG) gacha market — where players spend crypto to open randomised digital card packs — hit a record $36 million+ in weekly volume on April 13th, 2026, continuing the uptrend post the range-bound move in February. CARDS/USD, the largest tokenised trading card index, appears to be responding, surging 52% in the last 24 hours as on-chain card collecting sentiment recovers.