Hospital bills, captive patients: Why CCI’s ruling may weaken consumer protection | India News

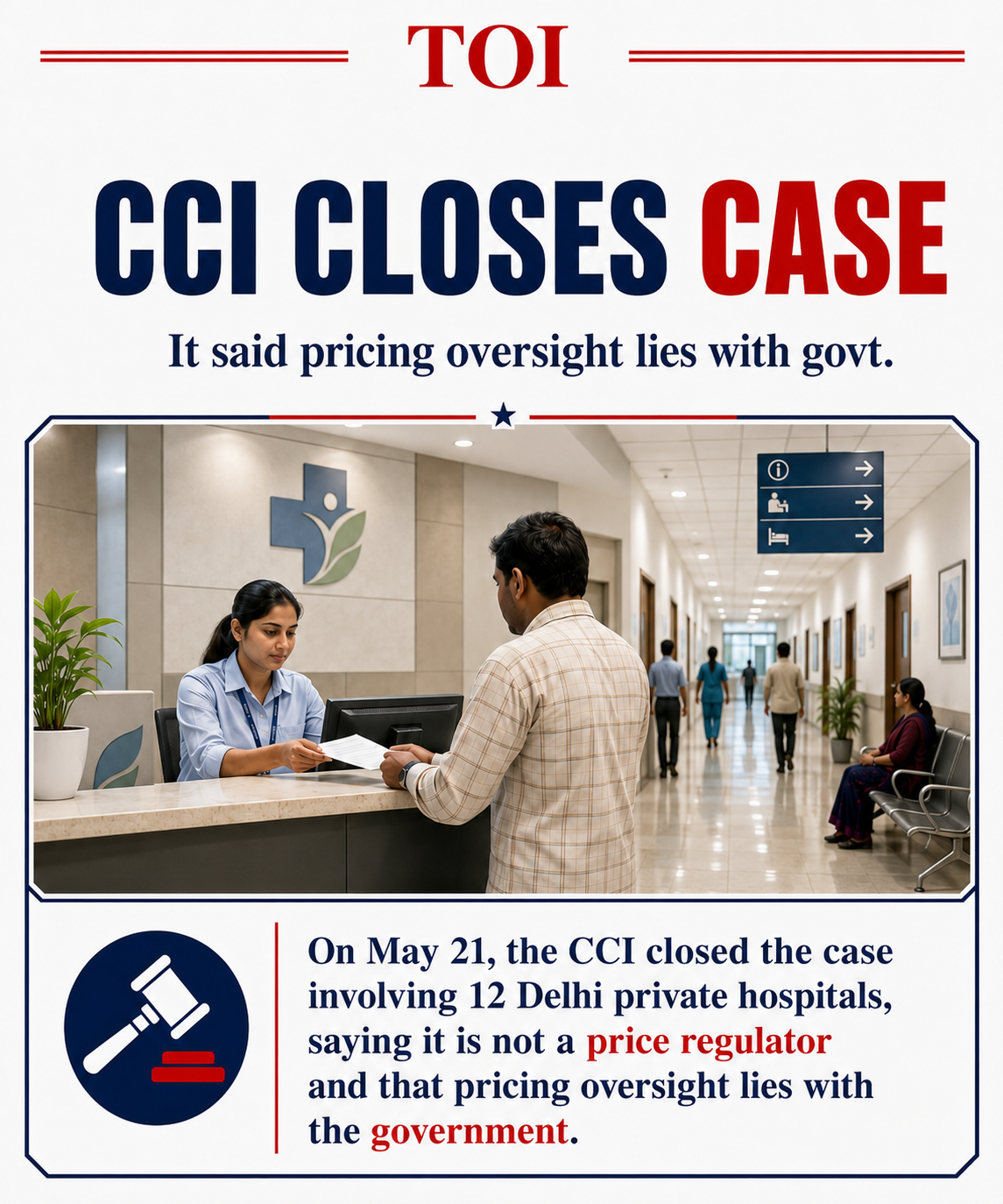

On 21st May, after a decade-long wait, the Competition Commission of India (CCI) absolved 12 Delhi-based super-speciality hospitals of allegations that they had subjected patients to exorbitantly marked-up healthcare charges. In what may prove to be a historic missed opportunity, the CCI effectively declined to intervene by holding that the regulation of healthcare pricing falls within the Government’s domain and that the Commission itself is not a price regulator. The ruling is not only legally questionable but also sets a troubling precedent where the CCI appears to have overlooked its preambular mandate to protect consumers in India’s $372-billion healthcare industry.The CCI is India’s only all-sector economic regulator that has the mandate of correcting abusive pricing and business practices of companies with dominant market power under section 4 of the Competition Act. The regulator can impose pecuniary penalties up to 10% of a company’s global turnover for the last three preceding financial years, besides imposing corrective behavioural remedies, including cease and desist orders.

From syringe pricing to hospital billing

The original complaint, filed in 2015, alleged that Max Super Speciality Hospital had colluded with disposable syringe manufacturers to inflate the retail prices of syringes sold through its in-house pharmacy far beyond the prices of identical products available in the open market. Although the CCI ultimately found no evidence of collusion between Max and syringe manufacturer Becton Dickinson, the investigation conducted by the Commission’s Director General (DG) led to a far broader inquiry into the pricing practices of Delhi’s leading private hospitals.

The probe expanded to examine mark-ups on medicines, consumables and diagnostic services charged to admitted patients across 12 prominent private hospitals, including six hospitals of the Max group, two belonging to the Fortis group, one operated by Apollo Hospitals, as well as Sir Ganga Ram Hospital, Batra Hospital and St Stephen’s Hospital. Significantly, Apollo, Fortis and Max are among the largest corporate players in India’s private healthcare sector.

What the pricing data showed

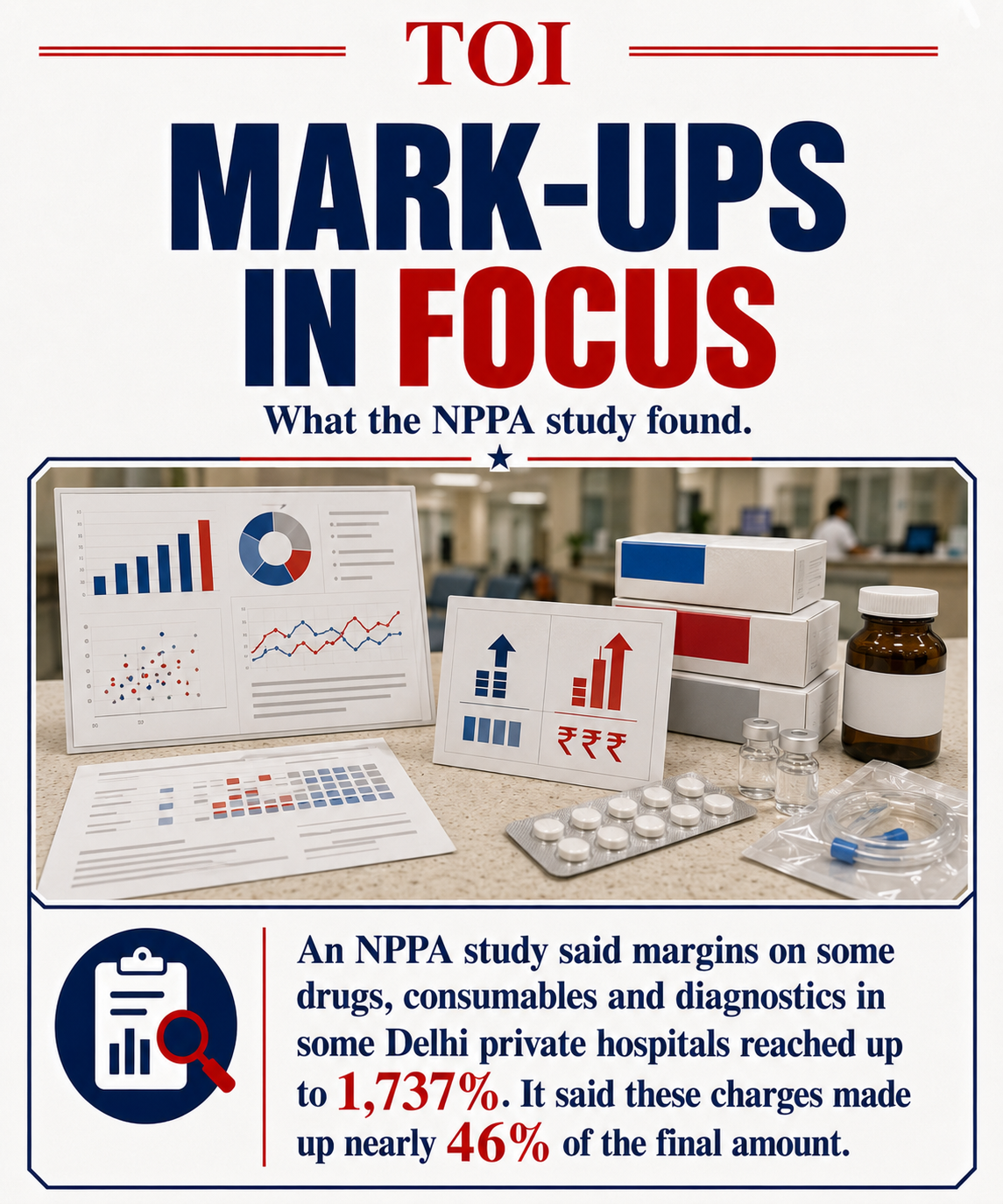

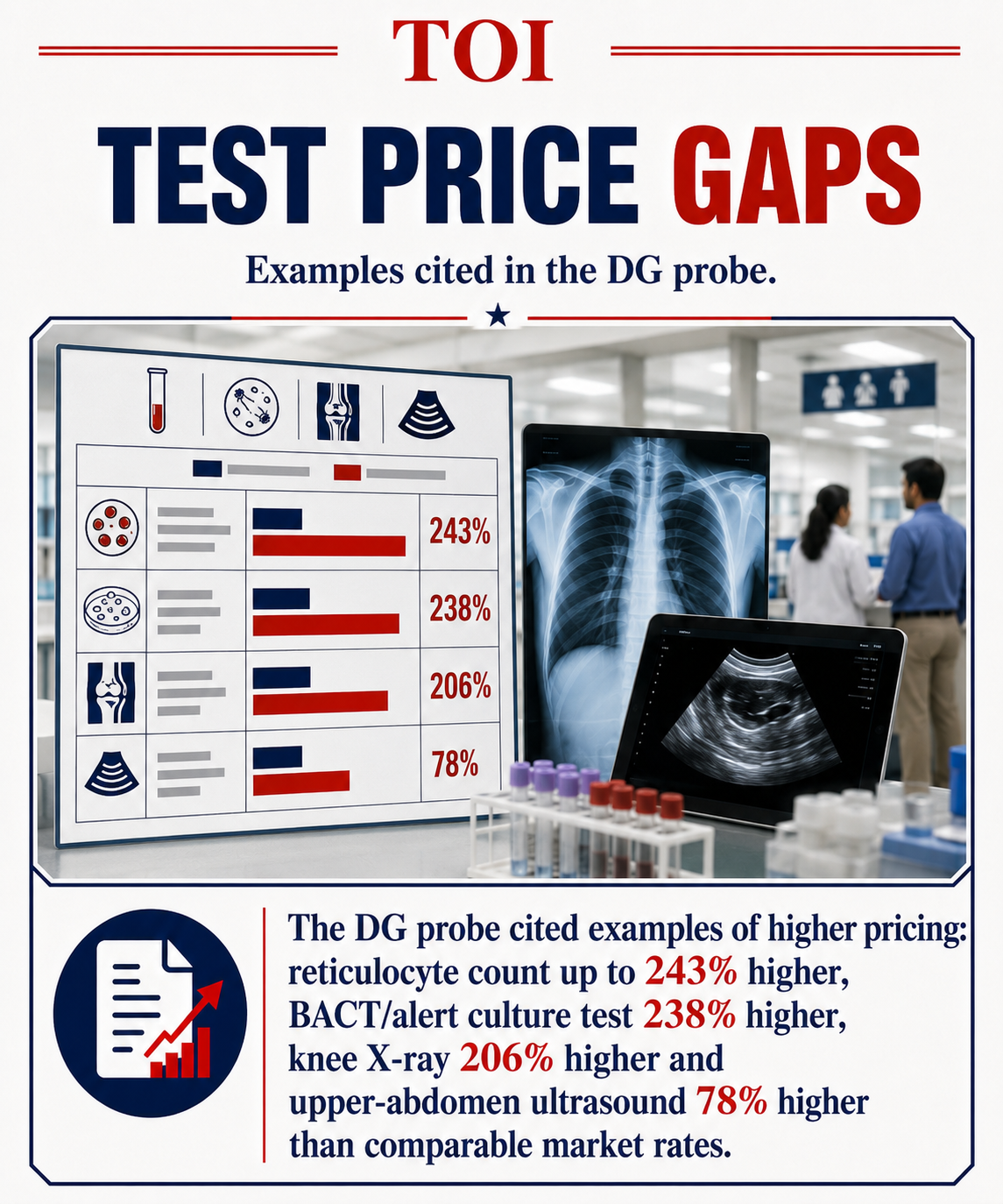

While the CCI was investigating the billing practices of Delhi’s leading private hospitals in 2018, a contemporaneous study by the National Pharmaceutical Pricing Authority (NPPA) revealed the scale of the problem. The study found that four of Delhi’s top private hospitals were earning margins of up to 1,737% on drugs, consumables and diagnostic services by requiring admitted patients to procure these products and services exclusively through in-house pharmacies.According to the NPPA, such charges accounted for nearly 46% of a patient’s final hospital bill. The Association of Indian Medical Devices (AIMED), an umbrella organisation of 300 device-makers, has alleged that Indian patients pay up to 25 times the factory or import cost of many medical devices when they are routed through private hospitals.Following a three-year investigation between 2018 and 2021, the DG identified several pricing practices across the hospitals under scrutiny, with the sole exception of St Stephen’s Hospital. For instance, the DG’s investigation found that for certain tests such as reticulocyte count and a BACT/alert aerobic culture test, Sir Ganga Ram Hospital charged up to 243% and 238% higher, respectively. Several ultrasound and X-ray procedures were similarly marked up between 50% and 200% above prevailing market rates.

The cost of a knee X-ray procedure at the hospital in 2018 was found to be 206% higher than at comparable standalone diagnostic centres, while an upper-abdomen ultrasound was priced 78% higher. The DG recorded similar concerns across other investigated hospitals.

The problem with CCI’s benchmark

Despite these findings, the CCI held that such pricing did not amount to excessive or unfair conduct. It argued that comparisons with standalone pharmacies and laboratories were inappropriate because hospital-based services operate under a different business model. However, this legal reasoning raises concerns. The central issue is not structural similarity across providers, but whether patients in a captive setting are being charged unjustified premiums.By limiting comparisons to similarly structured in-house systems, where similar pricing practices may be prevalent, the benchmark risks becoming circular and self-serving.

The captive patient problem

The economics of the sector support this concern. Hospitals operate in two interconnected markets: primary healthcare services and a secondary market comprising medicines, devices, consumables, and diagnostics. In practice, admitted patients have limited or no choice but to purchase these items through hospital-controlled channels, creating a structural “lock-in” that weakens price competition in the secondary market.The DG’s findings therefore pointed to a potential abuse of market power in this captive ecosystem, an issue of exploitative abuse under Indian competition law.

Can patients really make informed choices?

The CCI, however, rejected this view, arguing that patients are provided with pre-admission estimates and can make informed choices. It also found no evidence that patients are unable to assess overall treatment costs at the time of admission. This assumption sits uneasily with available evidence. A 2023 Public Health Foundation of India study found that 73% of patients are unable to understand their hospital bills.Common billing terms such as “consumables” and “disposables” often obscure actual charges, limiting price transparency. Recognising these concerns, the Supreme Court in 2025 urged state governments to address overpricing in private hospitals and curb mandatory in-house purchase of medicines and devices.The CCI also noted that patients remain free to switch to another hospital if they find the cost of in-house medicines or medical devices prohibitive. However, this reasoning appears to overlook the behavioural realities confronting patients and their families. In emergency or specialised care situations, where medical decisions are highly asymmetrical and time-sensitive, the notion that patients can exercise the same degree of informed economic choice as consumers in ordinary markets is deeply contestable.

Price control is not the same as competition enforcement

Finally, the CCI justified its decision by pointing to existing government regulation of pharmaceutical and medical device pricing, and by stating that it is not a price regulator. However, this conflates price control with competition enforcement of excessive pricing.First, while private hospitals in India operate under licences issued by state health departments, are registered with medical councils, and may seek accreditation from national healthcare quality bodies, none of these frameworks meaningfully regulate hospital billing structures or mark-ups on in-house services.

India’s weak transparency regime

The Clinical Establishments (Registration and Regulation) Act of 2010 (CEA) requires hospitals to display rates for procedures and medicines, maintain standardised records, and submit to periodic inspections. This is comparable in principle to the US Hospital Price Transparency Rules, under which hospitals are legally required to publish standard charges, negotiated rates, and discounted cash prices for items and services, making excessive mark-ups more visible to consumers and insurers.However, in India, 16 years after the adoption of the CEA, several states have not adopted the Act. The Act also has limited enforcement teeth. Indian hospitals that violate these transparency rules face minimal penalties. Besides, the Act does not provide patients with a clear statutory mechanism to seek redress for medical overbilling through consumer courts.India’s National Pharmaceutical Pricing Authority controls prices of essential drugs through the Drug Price Control Order, which is why a strip of paracetamol in India costs Rs 20 instead of Rs 200. However, the NPPA’s mandate does not extend to how hospitals mark up their in-house sale of medicines, devices or diagnostic services.

The question CCI should have asked

The CCI was not being asked to determine or fix prices for medicines, devices or diagnostic services. Rather, its mandate was to assess whether dominant hospitals had abused their market power through unfair pricing practices, an inquiry that falls squarely within the scope of Indian competition law. At its core, this ruling is not just about pricing disputes but about the limits of regulatory imagination in a market where patients have little real choice. When power meets opacity, outcomes matter. If competition law cannot protect captive consumers in healthcare, its promise of consumer welfare risks becoming hollow.Avirup Bose is Professor of Competition Law and Policy at Jindal Global Law School. He is a former expert consultant to the Competition Commission of India. Views are personal.